NOVEMBER/DECEMBER 2020 WAREHOUSING

A resilient

warehousing

strategy will

help a company

ride out any

unexpected

peaks or troughs

in demand

degree of confidence. However

lean or JIT a business is at point

of production, across the supply

chain, buffer stocks are back.

Inevitably, post COVID-19

businesses will be looking to build

far greater resilience into their

supply chains. This will call for

greater flexibility, enhanced agility

and most likely, higher levels of

inventory in the network.

Going forward, companies

need an intelligent strategy for

their warehousing requirements.

They know there will be peaks

and troughs in activity, although

they may vary in the confidence

with which they can predict either

timing or scale. They also know

that to use their own assets to

fully provision against short-term

peak demand is hugely expensive.

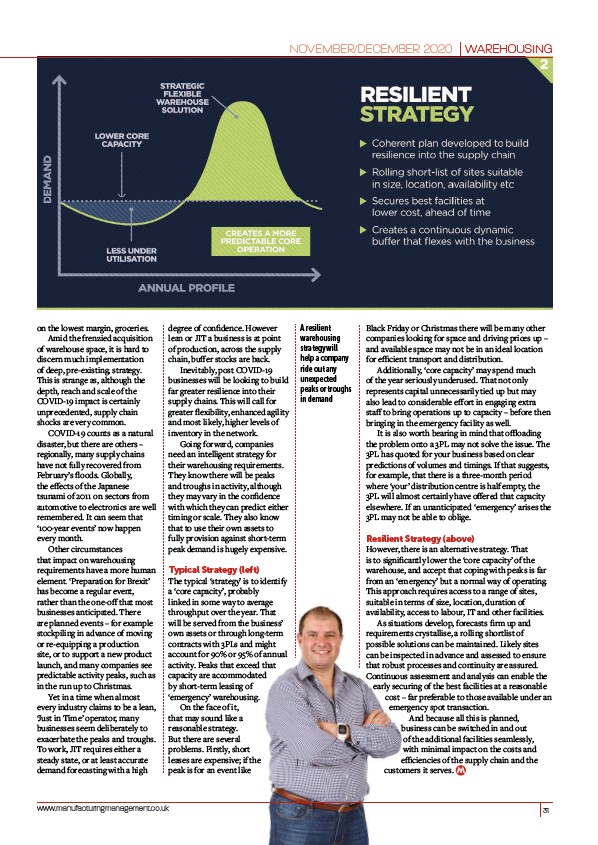

Typical Strategy (left)

The typical ‘strategy’ is to identify

a ‘core capacity’, probably

linked in some way to average

throughput over the year. That

will be served from the business’

own assets or through long-term

contracts with 3PLs and might

account for 90% or 95% of annual

activity. Peaks that exceed that

capacity are accommodated

by short-term leasing of

‘emergency’ warehousing.

On the face of it,

that may sound like a

reasonable strategy.

But there are several

problems. Firstly, short

leases are expensive; if the

peak is for an event like

Black Friday or Christmas there will be many other

companies looking for space and driving prices up –

and available space may not be in an ideal location

for efficient transport and distribution.

Additionally, ‘core capacity’ may spend much

of the year seriously underused. That not only

represents capital unnecessarily tied up but may

also lead to considerable effort in engaging extra

staff to bring operations up to capacity – before then

bringing in the emergency facility as well.

It is also worth bearing in mind that offloading

the problem onto a 3PL may not solve the issue. The

3PL has quoted for your business based on clear

predictions of volumes and timings. If that suggests,

for example, that there is a three-month period

where ‘your’ distribution centre is half empty, the

3PL will almost certainly have offered that capacity

elsewhere. If an unanticipated ‘emergency’ arises the

3PL may not be able to oblige.

Resilient Strategy (above)

However, there is an alternative strategy. That

is to significantly lower the ‘core capacity’ of the

warehouse, and accept that coping with peaks is far

from an ‘emergency’ but a normal way of operating.

This approach requires access to a range of sites,

suitable in terms of size, location, duration of

availability, access to labour, IT and other facilities.

As situations develop, forecasts firm up and

requirements crystallise, a rolling shortlist of

possible solutions can be maintained. Likely sites

can be inspected in advance and assessed to ensure

that robust processes and continuity are assured.

Continuous assessment and analysis can enable the

early securing of the best facilities at a reasonable

cost – far preferable to those available under an

emergency spot transaction.

And because all this is planned,

business can be switched in and out

of the additional facilities seamlessly,

with minimal impact on the costs and

efficiencies of the supply chain and the

customers it serves.

on the lowest margin, groceries.

Amid the frenzied acquisition

of warehouse space, it is hard to

discern much implementation

of deep, pre-existing, strategy.

This is strange as, although the

depth, reach and scale of the

COVID-19 impact is certainly

unprecedented, supply chain

shocks are very common.

COVID-19 counts as a natural

disaster, but there are others –

regionally, many supply chains

have not fully recovered from

February’s floods. Globally,

the effects of the Japanese

tsunami of 2011 on sectors from

automotive to electronics are well

remembered. It can seem that

‘100-year events’ now happen

every month.

Other circumstances

that impact on warehousing

requirements have a more human

element. ‘Preparation for Brexit’

has become a regular event,

rather than the one-off that most

businesses anticipated. There

are planned events – for example

stockpiling in advance of moving

or re-equipping a production

site, or to support a new product

launch, and many companies see

predictable activity peaks, such as

in the run up to Christmas.

Yet in a time when almost

every industry claims to be a lean,

‘Just in Time’ operator, many

businesses seem deliberately to

exacerbate the peaks and troughs.

To work, JIT requires either a

steady state, or at least accurate

demand forecasting with a high

Zstock /stock.adobe.com

www.manufacturingmanagement.co.uk 31

/stock.adobe.com

/www.manufacturingmanagement.co.uk