BRITISH STEEL JUNE 2019

TARNISHED STEEL

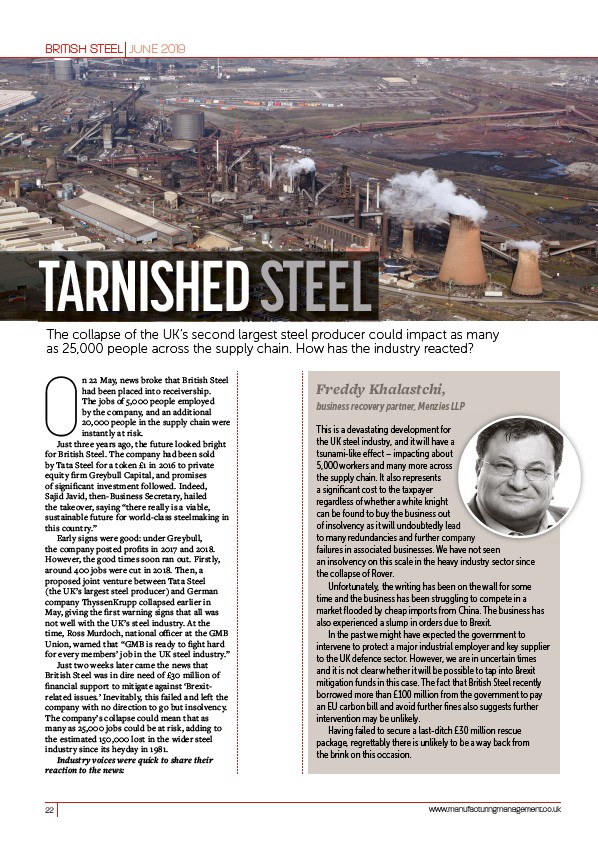

The collapse of the UK’s second largest steel producer could impact as many

as 25,000 people across the supply chain. How has the industry reacted?

On 22 May, news broke that British Steel

had been placed into receivership.

Freddy Khalastchi,

The jobs of 5,000 people employed

by the company, and an additional

business recovery partner, Menzies LLP

20,000 people in the supply chain were

instantly at risk.

Just three years ago, the future looked bright

for British Steel. The company had been sold

by Tata Steel for a token £1 in 2016 to private

equity fi rm Greybull Capital, and promises

of signifi cant investment followed. Indeed,

Sajid Javid, then-Business Secretary, hailed

the takeover, saying “there really is a viable,

sustainable future for world-class steelmaking in

this country.”

Early signs were good: under Greybull,

the company posted profi ts in 2017 and 2018.

However, the good times soon ran out. Firstly,

around 400 jobs were cut in 2018. Then, a

proposed joint venture between Tata Steel

(the UK’s largest steel producer) and German

company ThyssenKrupp collapsed earlier in

May, giving the fi rst warning signs that all was

not well with the UK’s steel industry. At the

time, Ross Murdoch, national offi cer at the GMB

Union, warned that “GMB is ready to fi ght hard

for every members’ job in the UK steel industry.”

Just two weeks later came the news that

British Steel was in dire need of £30 million of

fi nancial support to mitigate against ‘Brexitrelated

issues.’ Inevitably, this failed and left the

company with no direction to go but insolvency.

The company’s collapse could mean that as

many as 25,000 jobs could be at risk, adding to

the estimated 150,000 lost in the wider steel

industry since its heyday in 1981.

Industry voices were quick to share their

reaction to the news:

This is a devastating development for

the UK steel industry, and it will have a

tsunami-like e ect – impacting about

5,000 workers and many more across

the supply chain. It also represents

a signifi cant cost to the taxpayer

regardless of whether a white knight

can be found to buy the business out

of insolvency as it will undoubtedly lead

to many redundancies and further company

failures in associated businesses. We have not seen

an insolvency on this scale in the heavy industry sector since

the collapse of Rover.

Unfortunately, the writing has been on the wall for some

time and the business has been struggling to compete in a

market fl ooded by cheap imports from China. The business has

also experienced a slump in orders due to Brexit.

In the past we might have expected the government to

intervene to protect a major industrial employer and key supplier

to the UK defence sector. However, we are in uncertain times

and it is not clear whether it will be possible to tap into Brexit

mitigation funds in this case. The fact that British Steel recently

borrowed more than £100 million from the government to pay

an EU carbon bill and avoid further fi nes also suggests further

intervention may be unlikely.

Having failed to secure a last-ditch £30 million rescue

package, regrettably there is unlikely to be a way back from

the brink on this occasion.

22 www.manufacturingmanagement.co.uk

/www.manufacturingmanagement.co.uk